Did you know that in 2020 on an incremental basis, more deposits went to private banks in India instead of Public Sector Banks for the first time in history?

What is happening to the bad loan mess and NPAs that Indian banks have been forced to deal with by the RBI? Is the worst over?

Forced by the rapid pace of technology, can India’s gigantic banking system rapidly evolve to meet consumer demands? What’s stopping them?

In the latest episode of the Use Case podcast, Tamal Bandyopadhyay who has covered Indian banking for more than 2 decades, joins us to give us a lay of the land. His book, HDFC Bank 2.0 has been shortlisted for the Gaja Capital Business Book Prize 2020. He called his latest book ‘Pandemonium: The Great Indian Banking Tragedy’.

But we’ll leave it to you, the smart reader, to decide if the situation is that tragic.

You could read the text that follows or listen to the show on your favourite podcasting app here. Alternatively, check out the episode on Spotify here (26 min).

Introduction: Where India stands in the credit cycle today

Ravish: I was hoping that through this episode, I could learn a little bit more about the banking world from you, especially coming from the FinTech industry, it's important.

We often get so worked up about the startup world that we forget about the larger credit constructs that surround us on top of which we're supposed to build. So, starting from the basic - I want to begin by understanding where we stand in the credit cycle right now. To introduce our listeners to what a credit cycle is. A credit cycle usually mimics the economy, and there are 4 phases to it.

More context: Diagram of a typical credit cycle (source)

The first phase is the expansion phase where relatively easy lending standards are followed. We see increased borrowings in the market.

Then slowly as this happens, there is the downturn phase where companies begin struggling to meet their financial obligations due to stalled or negative growth. Banks start being more careful about who they lend to. So cheap capital is available only to tier one institutions.

Slowly and steadily, then the repair phase comes where as liquidity diminishes, companies start to fail and default rates rise. This leads to government being more concerned about having to repair balance sheets of banks, especially public sector banks while banks want to reduce costs and clean up their balance sheets.

We also see more asset sales, and then there is the recovery phase where the margins begin to improve, credit becomes better. Companies start to grow.

Then once that finishes, we again enter the expansion phase. Now at the risk of oversimplifying things, we saw parts of this credit cycle play out recently. Where do you think we are right now?

Tamal: You explained the credit cycle nicely and yes, I wish we were in the fourth phase that you mentioned.

In fact, we would have been in the fourth phase had there been no COVID.

Here’s what happened. We saw an expansion followed by cleaning up. While the banks were giving money for different reasons (in some cases they were under pressure from the government to extend not to a particular entity but to sectors, like infrastructure.) Also, we were seeing a corporate India, which did not exactly behave the way it should have.

And then as you know, there was a pressure from the Reserve Bank of India (on banks) to come up clean with- the so-called Asset Quality Review or AQR- a one of its kind tool globally that RBI introduced under Dr.Raghuram Rajan. What did AQR mean? It basically said that look I'm the regulator. I don't trust your accounting. You have been fudging. So I’ll send my own inspectors to check your books.

Even before that as part of the repair phase, RBI had also put in place the CRILIC database where almost on a real-time basis, banks were required to supply data to the regulator on all loans above certain criteria. That CRILIC data first gave the Reserve Bank of India an idea that, everything is not good because the same borrower is a bad borrower on a bank's book and a good borrower on another bank's books which means every bank was not following the rules.

And then RBI gave banks time to clean up their balance sheet in six quarters. If I remember correctly, it was between December, 2015 and March, 2017.

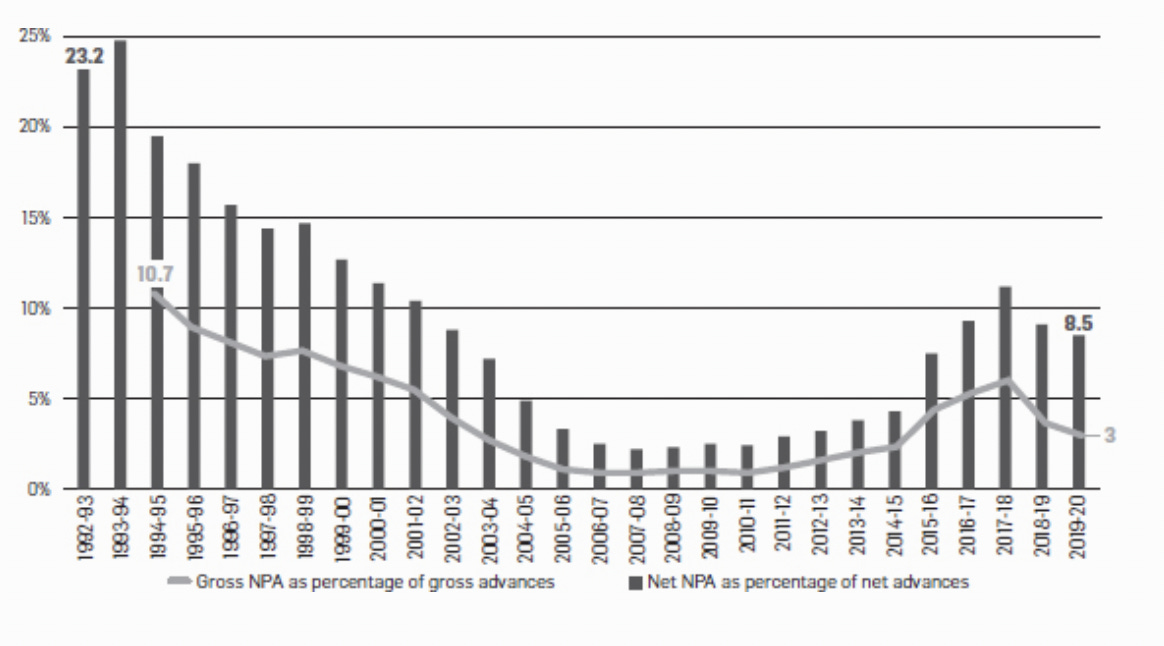

Mountain of NPAs: “The RBI’s war against bad loans led to a rise in the pile since 2016, after a long period of undereporting of NPAs by banks.”

Clever concealment: “Until 2015, banks were hiding their bad loans under restructured assets. The scene changed from 2016 onwards.”

Charts taken from: Tamal’s new book “Pandemonium: The Great Indian Banking Tragedy”)

Note that the IBC is not a great success story as of now, but what happened is this - IBC has given a threat to corporate India and at least made them come to the discussion table. Hence, ending March, 2020, you'll find a lot of bad loans got cleaned up, not through IBC, but outside IBC.

So as we were approaching March, 2020 we saw that the phase of recognition of bad loan was getting over. And the phase of recovery now starts.

The government came in and recapitalised the banks to the extent possible keeping in mind it’s fiscal strength. So that was a phase. At that time we thought, now this is the time for credit to pick up and the fourth phase that you are talking about in the credit cycle to begin. But instead COVID came and that has thrown all the calculation out.

We had a formal lock down and that affected business. Then the RBI came out with the moratorium. The moratorium was extended for 6 months. And then it was followed by a restructuring.

“Going by the Economic Survey 2019–2020, in 2019 every rupee of taxpayer’s money invested in PSBs, on average, lost 23 paise.” - Excerpt from “Pandemonium: The Great Indian Banking Tragedy”.

So it's a very fluid situation as of now. Banks have been talking about their Collection efficiency going up to 85, 90, 95, 97%. Things are not as bad as we had thought in April-May-June. Things are getting better, but I would not be convinced till I see the numbers of say March quarter.

Enjoying reading? Subscribe to the Turnaround newsletter to get more such insights, straight to your inbox. No spam- Ever!

Ravish: Right. I think it's very interesting what you said that banks are a little bit more risk averse, especially when it comes to unsecured loans. I personally am in the businesses of secured loans where we offer gold loans. So we did see a lot of bankers come up and say that because they have all this money that the RBI wants them to spend, it's better to give out gold loans instead than, say, unsecured loans.

But talking about RBI and the government wanting the banks to lend, there has been this controversy that the RBI gives capital to a lot of banks at a very cheap rate, but the banks go and park a bulk of that money back with the RBI. Is that true? Are the benefits that the RBI and the government coming up with actually being transferred to the people?

Tamal: You know yes and no. What the RBI has done is flooded the system with money. There is huge liquidity in the system. I just came from a holiday but about 8 days before the systemic liquidity was ₹7 trillion plus on a daily basis.

But what are the banks to do with that money tell me? Banks need to go back to the Reserve Bank of India and put the money at 3.25% - that is the reverse repo rate.

In fact, if you asked me, it (the capital) costs the banks probably more than 3.25%, because the average cost of deposits will not be 3.25%. It will be higher - Maybe 5% or something like that.

At this point of time, the reverse repo rate is the policy rate, not the repo rate, because banks are not taking money from RBI, banks are giving money to RBI.

Now is the bank passing on this benefit , to the borrowers? Yes. If you see home loans, they are at a historic low at this point of time.

Note: Tamal’s point about home loans got me thinking how this is one of the biggest markets waiting to be disrupted!

You are right in saying that banks are weary of unsecured loans. I know, particularly Small Finance Banks (SMBs) that are staying away from unsecured loans and are trying to rebalance their balance sheet with more secure loans and gold loan is a product which is now getting momentum and post COVID more so because gold price is going up. And the other reason is this people want money!

So, yes. And from the borrower's perspective too that cost of money has gone down. From the saver's perspective also. Now, that is a pretty bad situation.

Ravish: Yeah, with 7 trillion flooded into the system and inflation above 6%, whatever value their money is gaining, inflation is eating all of it anyway.

Tamal: Right. And I think it's the newly named negative return on your savings.

Ravish: What is also interesting is that in this time a lot of interesting products began to come up, especially by a lot of the FinTech players, different assets came up, not just Bitcoin, but digital gold for example.

Now - One particular topic that I want to move next towards (because a lot of FinTech companies are impacted by it) is how small banks have been impacted and what their position is right now compared to the big banks. Correct me but, RBI has different categories of banks, right?. Some Scheduled Banks and PSU for example, are too big to fail. So the RBI will always come and rescue them.

But for a lot of the small banks RBI took the stand that they will allow them to fail (wrong use of the word “fail” here – Tamal corrects it later! Also, I was referring to cooperative banks). A lot of the FinTech companies actually partner with these smaller banks because the big banks have their own mechanisms, digital platforms. Given that a lot of people listening to the show are working with these small banks, I would love to understand how the bigger players stand vs. the smaller ones.

Tamal: No offense intended but let me correct you on this because it's a very sensitive issue. RBI has never said that it will allow any bank to fail. In fact, since economic liberalisation in 1991, not a single Scheduled Commercial Bank has been allowed to fail.

No borrower has lost one rupee!

So what happened traditionally is when a bank was in trouble, RBI used to play the matchmaker- in the background, it would work out some kind of deal and primarily it worked out a deal with a Public Sector Bank.

The system changed in the 2 cases that happened this year. One is the case of Yes Bank and other is the case of Laxmi Vilas Bank.

In Yes Bank, it has not been matched with any one PSU entity. State Bank of India stepped in and picked up a stake. But along with the State Bank of India, came others like HDFC and Axis Bank and Kotak Bank, even Bandhan Bank which was born in 2015 - they came in and a package was worked out.

So, RBI has changed the way a bank is rescued. But RBI has never said a bank will be allowed to fail. This is particularly important because there is a category of banks which got a license in 2015-16, ~10 of them. They're called Small Finance Banks (SFBs). None of them will be allowed to fail.

I would think the banks, which need to reorient themselves or reinvent themselves are the larger banks, our public sector banks, because they are not tech savvy.

And now - I'm coming to your point, is this - Suddenly there is a lot of focus on technology in India. It reminds me how in the 1990s, Bill Gates when asked, in the context of banking said that banking will definitely remain relevant, but will the banks remain relevant? (The exact quote by Gates was “Banking is necessary, but banks are not”).

Again this does not apply for all banks, like for instance, State Bank of India digitally is pretty good. Bank of Baroda has been doing a lot of work in the digital space for the last few years, but not every public sector bank is digitally savvy. I think they need to ask themselves what to do? Because the millennial generation, if you want to retain them on the liability side, have their money as depositors and also get them on the assets side - they will not come to your branch.

Typically when you speak about public sector banks losing their market share, we say that their share is 70%. Now it's 65% or 63%, et cetera, BUT this is on the stock market. If you look at it from incremental basis in the past couple of years, their share in the market, both on the assets (their loan) and the live deposits, it is less than 20%. Less than 20%!

Saying people are happy keeping money with public sector bank - that's not correct. Every hundred Rupee deposits that are coming in to the banking system – 80/ 81/ 82 rupees are going to the private sector.

Ravish: That's very interesting. I want to just pause and absorb this. You're saying that a majority of the deposits, and I imagine you mean by volume, not by the number of depositors.

Tamal: Yes. Yes.

Ravish: Which is a very radical statement to make for a country that until now I thought was run by PSU Banks.

Tamal: No, no, no, no. This is because of technology. This is because of convenience. This is because of the shorter time it takes. So, this has already happened. And it's very fast, you know.They are losing their market share. As Mr. Nilekani said, what would have happened in years is now happening in weeks.

Ravish: That is a very interesting point. I'm going to go back and learn a bit more about this, but since you mentioned Mr. Nandan Nilekani, I want to mention an entire movement built around Open Credit Enablement Network or OCEN. In fact, just yesterday we had our first demo of account aggregators by Sahamti.

But let's stay on this topic of digital banking for a minute because there's a lot that has happened in this context. Let's first acknowledge that it is very difficult to build a digital piece for a bank. On an average, I read somewhere that there are around 100 to 200 IT systems involved in a bank. Even just for a small UPI payment, whether that be a rupee or one lakh ruppees, which is the UPA limit - it has to go through, 10ish odd systems or hops as they call it in the payment industry. And this happens in a matter of microseconds and if it fails at even one of these hops, that's a failure. It is challenging to build these big systems. And now all of these banks are working on legacy systems for a while. Staying on UPI, it is also built on IMPS. What is needed is a very, very radical change in technology. And is that even possible?

One thing, a lot of people said when HDFC was reprimanded by the RBI, that they would have fewer shutdowns if they moved completely towards cloud computing. But banks say that they can't move towards cloud computing until and unless for example, the data localisation law gives them more clarity on how to proceed. So what is the regulatory environment? Are there any impediments that are preventing this to happen?

Tamal: Yeah so HDFC bank has been pulled up by the regulator in this case. And it did happen earlier as well on one occasion with HDFC Bank. My understanding is, and I'm not privy to any confidential information but they're blaming the outage.

HDFC at the same time is also the most digitally savvy bank. If I'm not mistaken, 95% of its transactions are digital.

As far as the role of the regulator is concerned, I think the Reserve Bank of India is extremely progressive. Last week, they put up the thing where they're talking about loan given based on voice based sanction! And in the payment space, I think globally India is at the forefront.

Ravish: Google even recommend India's model to the US government, and NPCI is getting offers to go and build this stuff in Africa!

Tamal: Absolutely. Absolutely. So that's so it's the regulator which is playing a catalyst role. One thing that I, I don't think the regulator is coming in the way of innovation. I think many banks, particularly in the public sector, they are waiting to be disrupted. That's not a very happy story. That's just not a very happy story.

Ravish: I remember that in, in some of the papers on innovation theory there is this concept called “absorptive capacity”. What it essentially mean is, if you know how to ride a bicycle, it's easier for you to learn how to ride a motorbike.

A lot of what you're saying makes me think that some of the public sector banks, unlike HDFC or Axis Bank that have in the past put a lot of emphasis on digital banking , have failed to build the absorptive capacity in their internal systems, whether that was because of complacency or already owning distribution channels.

And hence lack those animal spirits that private sector banks have. Now in your new book, which is your sixth book, I think it's called Pandemonium: The Great Indian Banking Tragedy, you do cover a lot of other aspects and those that are more structural in nature. Could you walk us through some of the salient features that you highlight in the book?

Tamal: I have dissected various things in it - like one is the NPAs. How did we get into that mess? Who is responsible for that? There is a voice in even RBI that RBI was too aggressive. Then of course the story of the hyper active investigative agencies,

For example: One interesting story is the story of the MD and CEO of Allahabad Bank. It was her last day in office. Her farewell is being arranged in the boardroom. She was about to step out. And then from finance ministry, the mail comes at 4:53- you are sacked! So this is a story of how our bankers have been treated by the investigative agencies. Have the investigative agency been able to to prove culpability of these individuals? No, but they were sent to jail. (the connotation while Tamal was implying this was that the banks then became more and more risk averse as they fear investigative agencies to act against them for any bad loans.)

Another chapter is if the RBI also needs to change itself. My finding is that it does.

And then there are discussion of issues like how much time it takes between a CEO retiring and a new CEO coming in. There are gaps as much as nine months. Nine months you run a bank without a CEO in Andhra Bank's case. There is a gap of a 100 days for Bank of Baroda.

I wish I could name it the great Indian banking comedy! It's not a tragedy. It's actually a comedy.

Ravish: One would say that India's banking as well is just what, 60-70 years old (or young!) And a majority of private sector banking is even younger. Like 1993 was when HDFC- I think, correct me if I'm wrong, was set up.

Tamal: ‘94, yeah, all the new set of private banks are 25 plus year old. And if you talk about nationalization then 51 year old, (there are 200 year plus bank or like the State Bank of India) but post nationalization they are 51ish.

Ravish: So let's hope that as India’s banking system evolves (which is the foundation for a good economy) it shows resilience and it's no longer a tragedy…