SPACs a.k.a "Vegas Wedding Chapel of liquidity events"

SPACs a.k.a "Vegas Wedding Chapel of liquidity events"

IPOs, Private Equity and more with Gopal Jain, Gaja Capital

Once upon a time, long long ago…

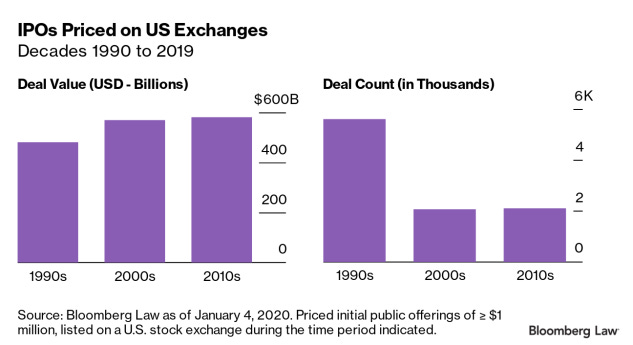

Starting a company and taking it to IPO was once regarded the holy grail in the world of startups and venture capital. The nineties saw 5,724 initial public offerings during its 10 years, a count that exceeds the IPO count for the next two decades—combined—by 1,455 offerings, or 34%.

But so much after the Dot Com bubble.

As our guest on the show this week, Gopal Jain, co-founder and Managing Partner at Gaja Capital, one of India’s biggest private equity firms, points out - “Since the dot com crash, and this was accelerated after the Global Financial Crisis (GFC), there has been a movement away from public markets in the US. We saw the phenomenon of private companies staying private for much longer. There was disenchantment with public markets.”

Ever since the start of the millennium, firms - especially tech companies, have managed to stay private for much longer. This was made possible by the greater availability of private money and the emergence of Venture Capital and Private Equity. That’s why the once mythical creature, the ‘unicorn’, is mythical no more.

The “disenchantment” with public markets that Gopal talks about, is largely to do with the way founders think about the valuation or pricing of their company. To understand why more and more founders (US based mostly) are not too keen on using the IPO (Initial Public Offering) route to go public, one needs to understand something called a “pop”.

Now, companies go public when they need more capital to grow and it is not available from the private markets (a.k.a ‘smart money’). They tell an investment bank, “Hey! I need X amount of cash”. The bank then arranges an investor road show for them and depending on the roadshow, an IPO price is determined. The bank commits to sell a few shares of their company to the investors at the determined price (let’s call it A).

Then, when the company is finally listed - in most cases, it opens at a price that can be different from the offering price. Let’s call this opening price as B.

Normally, B > A.

This (B-A) is what is called a “pop”.

But sometimes the opening price, B is lower than the offering price, A (like Uber last year). That indicates that the demand for the company’s shares is weak and that the investment bank didn’t correctly price the public market’s appetite. If the price isn’t stabilised in the 30 day stabilisation period by the investment bank, the stock can even go into a slide.

Either way, founders feel like they left money on the table and that their fate resides in the hands of the public completely. There is no certainty. Add to that, all the effort that they put in as part of the long drawn out IPO process could go down the drain. Not to forget, just to IPO you need to negotiate with several investors at the same time and that can be a pain in the ass.

But with SPACs, there is both certainty as well as speed.

Like what you’re reading? Do subscribe to our weekly newsletter! Get curated insights on start ups, product management and venture capital every Monday morning. No spam. Ever!

But what is it god damnit?

Special Purpose Acquisition Companies or SPACs are blank cheque companies set up and listed with the sole purpose of merging and taking another company public in the next 2 years or so.

Say a prominent investor like Chamath (whose judgement the public & institutional investors trust) decides to start a SPAC. He/she goes out and raises a certain corpus of capital which will be dedicated for the sole purpose of acquiring a company to take it public. Of that corpus the SPAC manager takes a certain cut for finding the right opportunity (about as high as 20% 😳).

This SPAC is already listed on the market. When it merges with the other company that wanted to go public, the combined entity then starts trading publicly under the company’s ticker.

Byrne Hobart called it “the Vegas Wedding Chapel of liquidity events”. It’s quick and easy unlike the traditional IPO. You negotiate once and your’e done.

For example: When Indian startup Yatra wanted to go public on the NASDAQ, it merged with a pre listed entity (SPAC) called Terrapin 3 Acquisition Corporation (which acquired 41.6% of Yatra’s common shares). Yatra needed the capital soon so they didn’t have the time to do a year long roadshow - so, it was just better to merge with a SPAC. Today Yatra trades on the NASDAQ under YTRA.

Now 2020, saw a record number of SPACs.

Research suggests that when markets are more volatile, companies tend to go public using SPACs. And god knows 2020 saw its fair deal of volatility and uncertainty (COVID, US elections, Brexit, etc…). In 2008 and 2009, approximately 31% of firms went public through a SPAC acquisition rather than through an IPO.

What’s behind the craze?

Former Facebook Inc. executive Chamath Palihapitiya is very open about why he’s such a fan of special purpose acquisition companies (SPACs), compared with taking a company public the usual way.

“In a traditional IPO you can’t show a [financial] forecast and you can’t talk about the future of how you want to do things, you’re just not allowed,” he said in a recent interview. He was referring to laws that exclude initial public offerings from so-called “safe harbor” protections covering forward-looking corporate statements. “Because the SPAC is a merger of companies, you’re all of a sudden allowed to talk about the future,” he told another YouTube questioner. “When you do that you have a better chance of being more fully valued.”

Unfortunately, there’s a danger that wildly optimistic financial forecasts are fueling a SPAC bubble, particularly among pre-revenue electric-vehicle companies and suppliers.

Source: Bloomberg Opinion

But wait, there are disadvantages to it!

SPACs aren’t exactly cheap. They’re actually more expensive than an IPO. As Bloomberg columnist, Matt Levine explains:

In an IPO, you typically pay investment banks a fee of 1% to 7% of the amount of money you raise, and you sell the stock to investors at a price that is probably too low; probably the stock will trade up by 10% or 20% or 100% on the first day that it’s public. People complain about both of these things—IPO fees and IPO pops—constantly; venture capitalists are always going around saying that the IPO process is broken and that something needs to replace it…

… The SPAC typically pays investment banks a fee of 5.5% of the money it raises, which is effectively passed on to the company that it takes public. It might also pay more investment banking fees for the merger with that company. It typically gives its sponsor—the famous investor or operator who runs the SPAC and finds a target company to take public—20% of its stock virtually for free, which, again, is passed on to that target company. So SPAC fees are about a quarter of the money raised, three or four times as much as you’d pay in an IPO, albeit better disguised.

Muddy Waters in one of its reports calls SPACs “present-day money grab” 😂

In the great present-day money grab known as SPAC promotion, egregious mistakes will be made – such as missing an impending customer defection that could cost ~35% of revenue within two years. A business model that incentivizes promoters to do something – anything – with other people’s money is bound to lead to significant value destruction on occasion. That’s even more true when a SPAC buys a business from the fourth consecutive private equity group to have owned it. C’mon, man.

But then again, the argument in favour of SPACs goes that they have evolved over time and the SEC has put in place greater scrutiny. A retail investor is also trusting the goodwill of the SPAC manager to do what is right.

As a lot of Indian late stage tech companies look for more growth capital - I wonder how many might consider SPACs a legitimate option to raise money. Will we see the Yatra story repeat in these unprecedented times?

We’ll soon find out.

As part of our Gaja Capital Business Book Prize series, one of our most interesting discussions on the podcast, was with Gopal Jain, who as a growth investor has seen several IPOs in the 15 years since co-founding Gaja Capital (which by the way, also put in ₹204 Cr into Sachin Bansal’s Navi Technologies). Do check out the episode with Gopal on your favourite podcasting app. We talk about not just SPACs, but also growth investing, the private equity landscape and more.